Make before you break: China's financial lessons from global climate fight

Make before you break: China's financial lessons from global climate fight

While the old saying suggests "there is no making without breaking," Chinese policymakers decided to take another route.

In retrospect, 2022 was a year of unprecedented extreme climate events: floods in Pakistan, wildfires in Europe, and record-breaking heatwaves in many parts of the world, which affected millions of people, cost billions of dollars, and sent clear warning signs that climate change is here.

There was more bad news. Despite some encouraging progress in policymaking and agreement signing, the global climate action was overshadowed by the plumes puffed from European coal-fired plants that reopened after the Ukraine crisis led to an energy crisis.

Though not directly affected by the energy crunch, China has found the backtracking on climate action equally alarming. Aiming at carbon neutrality by 2060, the country has been closely watching for lessons to build up its own solutions.

The country's financial and monetary policymakers are among the keenest watchers. Xuan Changneng, vice governor of China's central bank, has cautioned against the calls for "lightning-like" carbon reduction. Some financial institutions have simply suspended financing all activities related to coal power generators.

In China, where resource restraints and the stage of economic development have made its low-carbon transition a more challenging task, some regions also tend to take aggressive actions when promoting energy transition, he warned at a forum in December.

Though the old saying suggests "there is no making without breaking," Chinese policymakers, upon lessons learned from domestic and overseas experiences, have decided to take another route: make something new before they break the old.

It is a principle that goes in line with the country's basic tone for economic work -- seeking progress while maintaining stability, according to Xuan.

"Low-carbon transformation is no walk in the park," Liu Dechun, an official with the National Development and Reform Commission (NDRC), China's top economic planner, expressed similar concern when commenting on the setbacks in global carbon reduction efforts.

Reducing emissions is neither reducing productivity nor stopping the emission, but rather integrating carbon goals into the big picture of environmental protection and economic and social development, Liu has said.

THE ART OF BALANCING

Balancing has always been a substantial part of policymaking.

In a key document guiding China's work toward its carbon goals released in 2021, the NDRC stressed the need to balance efforts to reduce pollution and carbon emissions with the need to ensure the security of energy, industrial chains, supply chains, and food, as well as normal daily life.

"We need to respond appropriately to any economic, financial, and social risks that may arise during the green and low-carbon transformation to prevent any excessive response and ensure carbon emissions are reduced in a safe and secure way," it said.

Wang Xin, director-general of the Research Bureau of the People's Bank of China (PBOC), has discussed the impact of carbon neutralization on the macro-economy and central bank policymaking.

"The impact of policy tools chosen for carbon reduction on the macro-economy and financial markets could be far greater than climate events themselves," he wrote in a co-authored working paper published in December 2021.

To fulfill the carbon goals, China needs to work on emission cuts and carbon offsetting, according to Wang. Both directions require proper coordination of fiscal, financial and industrial policies to guide funds into green sectors, a process that will affect China's productivity, inflation, employment and economic and financial stability profoundly.

The short to medium-term and long-term impacts of low-carbon transition on the Chinese economy varies, Wang wrote, citing academic research. For instance, in the short run, cutting emissions by restricting certain industries will affect industrial output and to some extent drag down economic growth, but this could be solved by upgrading industrial structure.

Financial institutions are also prone to be affected by climate change and low-carbon transition, as a significant part of their assets are loans to carbon-intensive industries, according to PBOC's Xuan.

Withdrawing from carbon-intensive assets too quickly would add to transition risks, while slow withdrawal would both hamper carbon goals and give rise to financial risks, Xuan said. Therefore, financial institutions should, under regulatory guidance, improve their capabilities in green finance to support the economic transition.

MAKE BEFORE BREAK

To promote green and low-carbon transition, according to Wang, a central bank can focus on two directions in promoting the green and low-carbon transformation of the economy: encouraging long-term financing for energy transition and reducing investment uncertainty with clear and predictable measures.

In terms of monetary policymaking, he said, appropriate monetary policies could ease the potential shocks of climate change and low-carbon transition, and structural monetary policies can encourage financial institutions to develop green finance businesses.

Support should be given to eco-friendly industries and advanced production capacity, but only to the extent that it does not hamper price targets, he said.

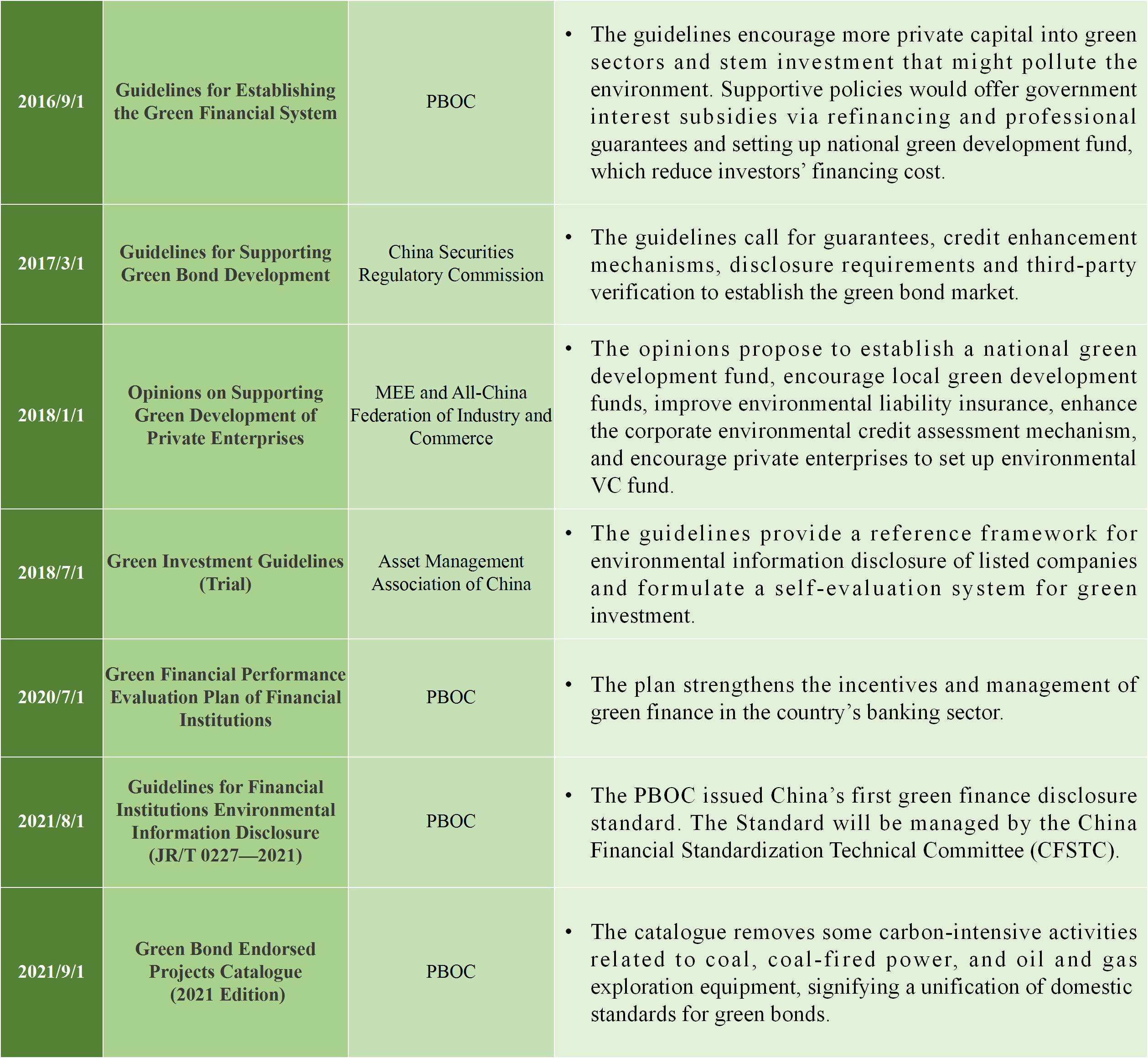

Toward this end, in 2016, the PBOC led cross-department coordination to introduce a guideline on building a green financial system, which is the world's first green financial policy framework approved and established by central government departments.

Under such a framework, the issuance of green financial products boomed. By the end of 2021, outstanding green loans in yuan and foreign currencies reached 15.9 trillion yuan (about 2.34 trillion U.S. dollars), jumping 33 percent from the previous year.

Given China's coal-dominated energy resource endowment, besides green finance, China has included transition finance into a broader range of innovative financing options to address climate change.

While green finance focuses mainly on minimum pollution or emission activities like clean energy, transition finance provides financing to projects related to carbon-intensive industries, such as carbon trading, to fund their transition to decarbonization.

In 2021, the PBOC introduced two structural monetary policy tools to encourage more social funds into the green and low-carbon sectors: the carbon-reduction credit facility and the special re-lending tool for promoting the clean and efficient use of coal.

By March 2022, the PBOC has supported financial institutions in issuing over 240 billion yuan of loans through such two tools, with the carbon-reduction credit facility helping cut emissions by 47.86 million tonnes of carbon dioxide equivalent, central bank data showed.

The financial support did pay off. The proportion of clean energy sources in China's total energy consumption increased from 14.5 percent in 2012 to 25.5 percent by the end of 2021, gradually replacing coal. The country also leads the world in manufacturing clean energy facilities for wind and photovoltaic power.

"Carbon peaking and neutrality is never just a matter of carbon," NDRC Director He Lifeng wrote in an article in 2021. Rather, according to him, it is an economic and social systemic change and a fight that should never be fought alone.