💖 Yuan's path toward a global currency

💖 Yuan's path toward a global currency

"Do not bet on one-way appreciation or depreciation of the yuan. Gamblers will definitely lose in the long run."

Walk steadily to reach far.

—— The Book of Rites

Lingering COVID-19 pandemic, rampant global inflation, danger of worldwide economic slowdown, an energy shortage to be alleviated and the Federal Reserve's hawkish rate hikes have created huge uncertainty in the international financial market.

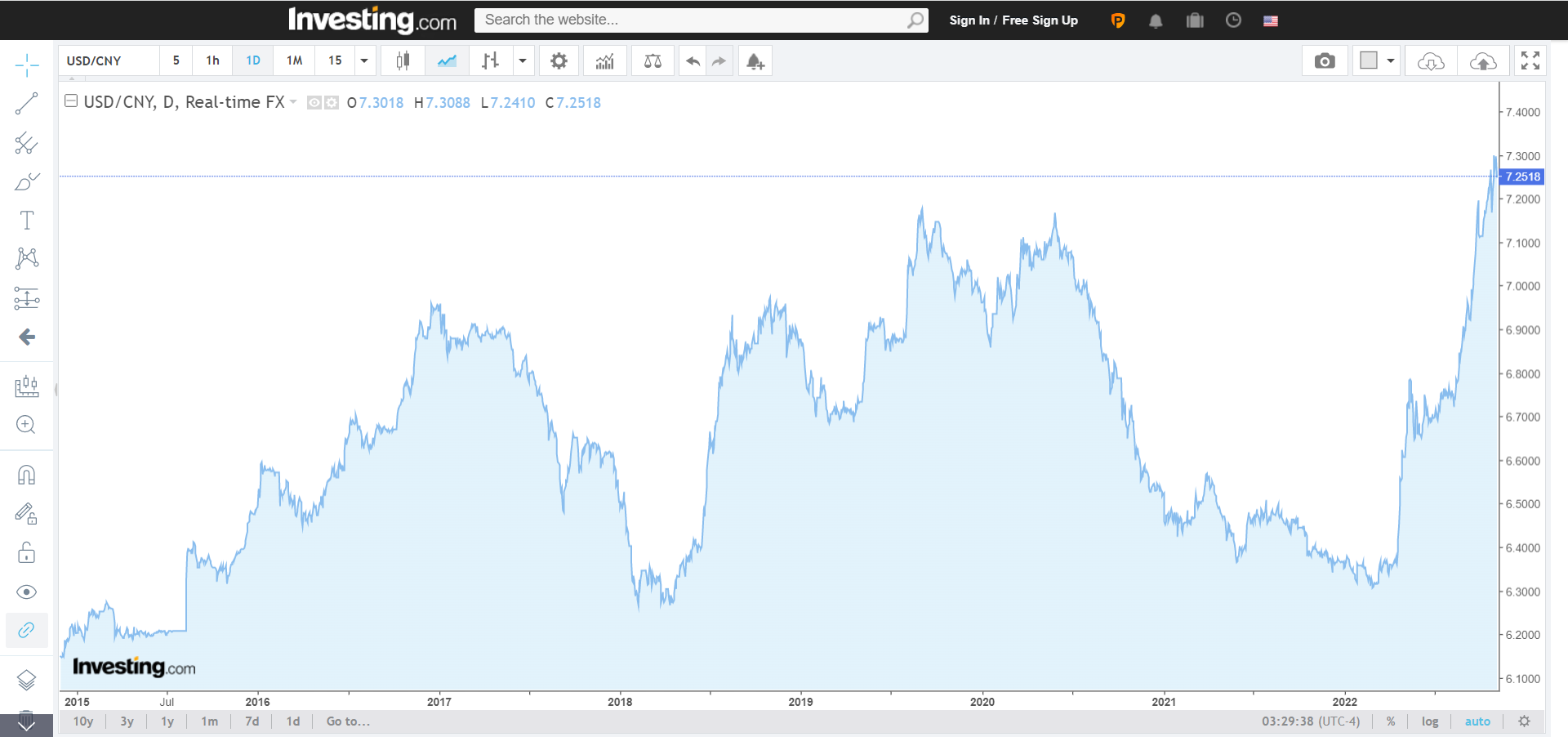

On the foreign exchange front, multiple currencies have to grapple with the downward pressure imposed by a stronger U.S. dollar. China's currency, the yuan or renminbi (RMB), has depreciated by more than 10 percent against the greenback this year.

DEFENDING YUAN

The People's Bank of China (PBOC), has been decisive in defending the yuan. In a strongly-worded statement made in late September, the central bank warned against betting on single-sided fluctuation of the currency.

"Do not bet on one-way appreciation or depreciation of the yuan," it said. "In the long run, gamblers will definitely lose."

On Oct. 28, central bank governor Yi Gang emphasized the need to strengthen expectations management and make the yuan's exchange rate more flexible when delivering a report at the 37th session of the Standing Committee of the 13th National People's Congress, China's top legislature on financial work.

"Over a period of time in the future, our country has the condition to continue with a normal monetary policy and keep the yuan's value stable as long as possible," he said.

On Nov.2, Yi made a speech via video at the Global Financial Leaders' Investment Summit held by the Hong Kong Monetary Authority. He said that the RMB exchange rate will continue to remain relatively stable at a reasonable and appropriate level, maintaining its purchasing power and keeping its value stable.

Despite the short-term volatility, Chinese authorities have stayed confident about the secular strengthening trend of the yuan and its growing market status, as a rising economy is bound to result in a stronger currency. Meanwhile, policy maneuvers have been on the go.

Last month, China raised a macro-prudential adjustment parameter from 1 to 1.25, a multiplier that decides the upper limit of outstanding cross-border financing an institution can have, to allow companies and financial institutions to borrow more foreign debt. In September, the central bank cut the foreign exchange reserve requirement ratio for financial institutions by 2 percentage points.

Zhang Jingjing, macro analyst with the China Merchants Securities, was impressed by "the full measure of composure" of the central bank in tackling with the yuan's downward trend.

Compared with its two previous rounds of marked depreciation, each lasting about four months in 2015 and 2018 respectively, the yuan has shown more firmness and resilience.

In terms of exchange rate expectations, Zhang has seen no basis for persistent depreciation of RMB exchange rate after taking into consideration the country's cross-border capital flows, external debt pressure, foreign exchange reserves, enterprises' exchange rate risk management as well as the central bank's policy toolkit.

It is worth noting that major currencies have all weakened against the U.S. dollar and the yuan's depreciation so far has been much less than others.

Data from the International Monetary Fund (IMF) showed the dollar is at its highest level since 2000, having appreciated 22 percent against the yen, 13 percent against the Euro and 6 percent against emerging market currencies since the start of this year.

NO HASTE IN GOING GLOBAL

Despite recent volatility in its exchange rates, the yuan has witnessed growing popularity and broader international use over the years.

Chinese yuan has now become the fifth most traded currency in terms of global foreign exchange turnover, with a market share of 7 percent, says a report from the Bank of International Settlements.

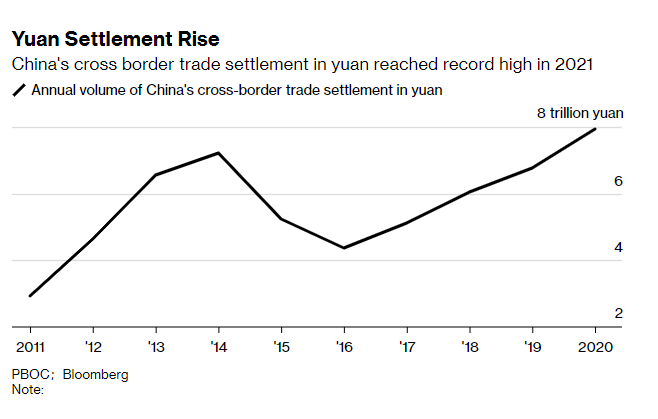

A separate report from the PBOC on the internationalization of the yuan also gives positive indicators. China's cross-border RMB receipts and payments in non-banking sectors jumped by 15.2 percent year on year to 27.8 trillion yuan from January to August.

The share of securities investment in cross-border RMB receipts and payments surged 30 percent in 2017 to around 60 percent in 2021. Since 2017, RMB bonds have been included in three international bond indexes.

Thanks to the diversification trends of reserve assets and the inclusion of the renminbi in the IMF's SDR basket, the world's central banks have become more willing to hold renminbi reserves.

Since currency internationalization tends to be a long-term process, Chinese analysts maintain that the yuan will have to follow its natural course to become a global currency. A steady-and-no-hasty approach has been advocated.

At present, there is no immediate need for the renminbi to become an international currency.

——Xiao Lisheng, financial expert with the Chinese Academy of Social Sciences

The speed of currency internationalization depends on many factors from an economy's overall strength to the acceptance and use of its currency by other countries.

Remarkable progress has been made in the internationalization of the renminbi since China promoted cross-border renminbi settlement in 2009, but yuan's shares in international transaction, pricing, clearing and global forex reserves remain fairly limited, and there is still much room for improvement, Wang Yongli, general manager of China International Futures Co.,Ltd., was quoted as saying by the Economic Observer.

In the next stage, the central bank report noted that China will steadily and prudently boost the internationalization of RMB, conform to market-driven principles and respect the choices of market entities.

It will continue to improve the policies and infrastructure for the cross-border use of the yuan and well meet the need from the real economy. Specific policy priorities are as follows:

Facilitating the two-way opening-up of financial markets at a higher level, and promoting a virtuous circle between the onshore and offshore RMB markets.

Continuing to improve the macro-prudential management framework and optimize the monitoring, assessing and early warning mechanism for the cross-border capital flows, so as to safeguard the bottom line that no systemic risks should occur.

Improving the liquidity of renminbi-denominated assets, simplifying the process for foreign investors to enter the Chinese market, and enriching the types of investable assets.

Expanding cooperation on local currency settlement with the ASEAN countries and neighboring countries, promoting direct trading between RMB and relevant currencies, and supporting other countries and regions in developing local RMB foreign exchange markets.

Improving the offshore RMB liquidity supply mechanism and giving full play to the positive role of clearing banks in cultivating the offshore RMB markets.

| A guest post by

|